A Bank With a Negative Interest-sensitive Gap

This means that an increase in market interest rates could cause a decline in net interest income. A defensive strategy can be applied to eliminate an adverse banks interest-sensitive gap.

Negative Gap Overview Example Effects Formula

If a bank has a negative interest-sensitive gap one of the possible management responses would be to.

. A Has a greater dollar volume of interest-sensitive liabilities than interest-sensitive assets. Any liquidity gap generates an interest rate gap. Liability sensitive positive gap rising rates lead to a decline in NII.

Wait for the interest rates to fall or be stable. If a bank has a negative gap the amount of liabilities repricing in a given period exceeds the amount of assets repricing during the same period thus decreasing net. If a bank has a negative interest-sensitive gap one of the possible management responses would be to.

Assuming that one-year rate-sensitive assets and liabilities are 50 and 70 million euros respectively and that the bank expects a rise in interest rates over the coming year of 50 basis points 051 the expected change in the NII would then be. If there is no liquidity gap the fixed rate gap and the variable rate gap are identical in absolute values. C Will generate a higher interest margin if interest rates fall.

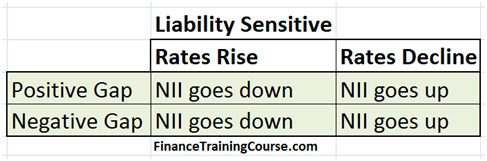

A bank with a negative interest-sensitive GAP. Conversely a positive or asset-sensitive gap occurs when assets exceed liabilitys in a given time band. Is immunized against interest rate changes.

B Will generate a higher interest margin if interest rates rise. A bond has a duration of 75 years. A negative or liability-sensitive gap occurs when liabilities exceed assets in a given time band.

Gap analysis measures the difference between the amount of interest-sensitive assets and interest-sensitive liabilities that will reprice on a cumulative basis during a given time horizon. Excess funds will be invested or deficits will be funded at a future date at an unknown rate. B Will generate a higher interest margin if interest rates rise.

In our example if the interest rate on liabilities increases the bank has to pay out more in interest. B Will generate a higher interest margin if interest rates rise. Wait for the interest rates to fall or be stable.

Since in a negative gap the interest-sensitive assets are less than the interest-sensitive liabilities there exists a risk in that if the interest rates rise there will be losses as the banks net interest margin will reduce. After incorporating the impact of the rising interest rate NII declines to 1365 million. If market interest rates increase things could get bad for the bank.

A negative gap is not necessarily a bad thing because if interest rates decline the banks liabilities are repriced at lower interest rates. Aggressive gap management could be bad for shareholder wealth despite increasing net interest income in the short term due to interest rate risk especially on the asset side. If a bank has a negative interest-sensitive gap one of the possible management responses would be to.

A Has a greater dollar volume of interest-sensitive liabilities than interest-sensitive assets. A negative gap is a situation where a banks interest-sensitive liabilities exceed its interest-sensitive assets. If a bank has a negative interest-sensitive gap one of the possible management responses would be to.

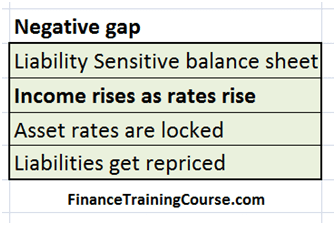

A bank with a negative interest-sensitive GAP. Negative gap is often associated with positive gap which occurs when the banks assets exceed its liabilities. A negative gap is a situation where a banks interest-sensitive liabilities exceed its interest-sensitive assets.

FIGURE 231 Interest rate gap. A negative gap or a ratio less than one occurs when a banks interest rate sensitive liabilities exceed its interest rate sensitive assets. Deutsche Bank The pitfalls of aggressive gap management.

Interest Rate Gap and Liquidity Gaps. A Has a greater dollar volume of interest-sensitive liabilities than interest-sensitive assets. Will generate a higher net interest margin if interest rates fall.

Value of a possible negative gap or increase the size of a possible positive gap and vice versa. Wait for the interest rates to fall or be stable. The interest rate risk traditionally measured by the difference between assets and interest-sensitive liabilities gives a report on the banks situation at a certain point in time.

Changing the interest rate may determine the amount of revenue earned by reflecting in the balance sheet the value of the banks assets and liabilities. A bank with a negative interest-sensitive GAP. If management expects interest rates to vary up to 4 percent during the upcoming year the banks ratio of its 1-year cumulative GAP absolute value to earning assets should not exceed 25 percent.

Because the banks interest-rate sensitive liabilities exceed its interest-rate sensitive assets by 30 million the bank has a negative gap. Will generate a higher net interest margin if interest rates rise. E A and C.

Negative gap is a term used to describe a situation in which a banks interest-sensitive liabilities exceed its interest-sensitive assets. C Will generate a higher interest margin if. D A and B.

Our base started off with an NII estimate of 159 million. A bank with a negative interest-sensitive GAP. A bond has a duration of 75 years.

Example of positive duration gap asset sensitive bank Source. An important formula to understand is the interest rate gap which is the difference between interest-bearing assets and. Wait for the interest rates to fall or be stable.

As predicted on a liability sensitive balance sheet with a positive gap as interest rates rise NII will decline. The bank will risk changes in NIM equal to plus or minus 20 during the year Hence NIM should fall between 4 and 6.

Asset Liability Mismatch Asset Liability Management Asset Liability

Asset Liability Mismatch Financetrainingcourse Com

Asset Liability Mismatch Financetrainingcourse Com

Comments

Post a Comment